Spam texters who send unsolicited messages have close links to payday lenders, a Sunday Post probe has discovered.

Bosses at three of the UK’s largest payday lenders Wonga, Quick Quid and Mr Lender denied using nuisance texts to get new customers at a House of Commons grilling from the Business, Innovation and Skills Committee.

But a Sunday Post investigation has uncovered close ties between the payday firms and a network of broker companies who send out spam messages and then pass on their details to the money lending firms who charge up to 10,000% APR.

Those “leads” can change hands for up to £60 a time, double the cost of a potential mortgage customer and showing how lucrative the business of payday lending is.

The industry is now worth an estimated £2 billion a year and has doubled in size in just three years.

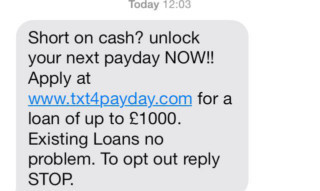

Our investigation started after we were sent unsolicited texts to our TPS-registered phones by broker firms.

When we responded we were inundated with offers of cash after filling in online forms. Often the offers were from broker firms who made their money by introducing us to lending companies.

Within just 48 hours we received 35 text messages, five emails and three phone calls offering to lend vast sums of cash. Although we asked for just £160, we were offered up to £1,500.

But the huge loans in time for Christmas came at a cost horrific interest.

One firm said our £160 loan would need to be paid back at a whopping 9,986% APR. Most were in excess of 2,000%.

After filling in their online form, one of the firms who sent us unsolicited texts redirected us to the website of payday giants Wonga who came under fire yesterday after it emerged they had offered a £400 loan to a 13-year-old schoolboy.

The same broker also put us in touch with US-based Quick Quid via an Indian firm.

In one of our applications, under a fake name, we ticked a box that should have meant our details were not passed on to third parties.

But that plea was ignored, breaking the Privacy and Electronic Communications Regulations law, and we were soon plagued with more loan offers for our invented applicant.

Mike Crockart, the Edinburgh West MP who sat on the committee which questioned the practices of the payday industry, said: “It’s all very well for payday lenders to say they don’t make calls or send texts, but the leads have come from somewhere.

“They must take responsibility for ensuring the details have been obtained legally otherwise all they are doing is outsourcing the nuisance while still making money from them.”

We contacted the payday lenders but none of them got back to us.

A spokesperson for the ICO, who regulate telemarketing, said: “The ICO is currently carrying out an extensive investigation into spam texts. We are unable to disclose any further details.”

They added payday loan companies were one of the biggest sources of complaints.

Earlier this week, Citizens Advice Scotland claimed payday loan companies had failed to deliver on pledges to clean up the industry.

The High Street lenders launched a code of conduct a year ago but a survey of people seeking help at Citizens Advice Scotland offices said they’ve broken most of their promises.

WHAT THEY SAID TO MPs EARLIER THIS MONTH

Adam Freeman (Mr Lender): “We would never randomly text somebody, ‘Do you need a loan? Come to Mr Lender.’ No, we have never purchased lists or done anything like that.”

Henry Raine (Wonga): “We do not text people as a way of getting business. The day before payment date, we will use a text to say, ‘Just to remind you that your money is due’, so it is not a PPI-type situation where we are all getting texts the whole time. We do not do any of that.”

Andy Lapointe (Quick Quid): “You would have to opt in to receive texts from us.”

Enjoy the convenience of having The Sunday Post delivered as a digital ePaper straight to your smartphone, tablet or computer.

Subscribe for only £5.49 a month and enjoy all the benefits of the printed paper as a digital replica.

Subscribe