WHEN it comes to credit cards, managing debt is consumers’ top priority, a new report has revealed.

MoneySuperMarket analysed two million enquiries from its Smart Search eligibility tool to reveal what Brits look for most when searching for a credit card.

More than 100 credit cards were grouped into four categories to represent how they are typically used.

Credit card types

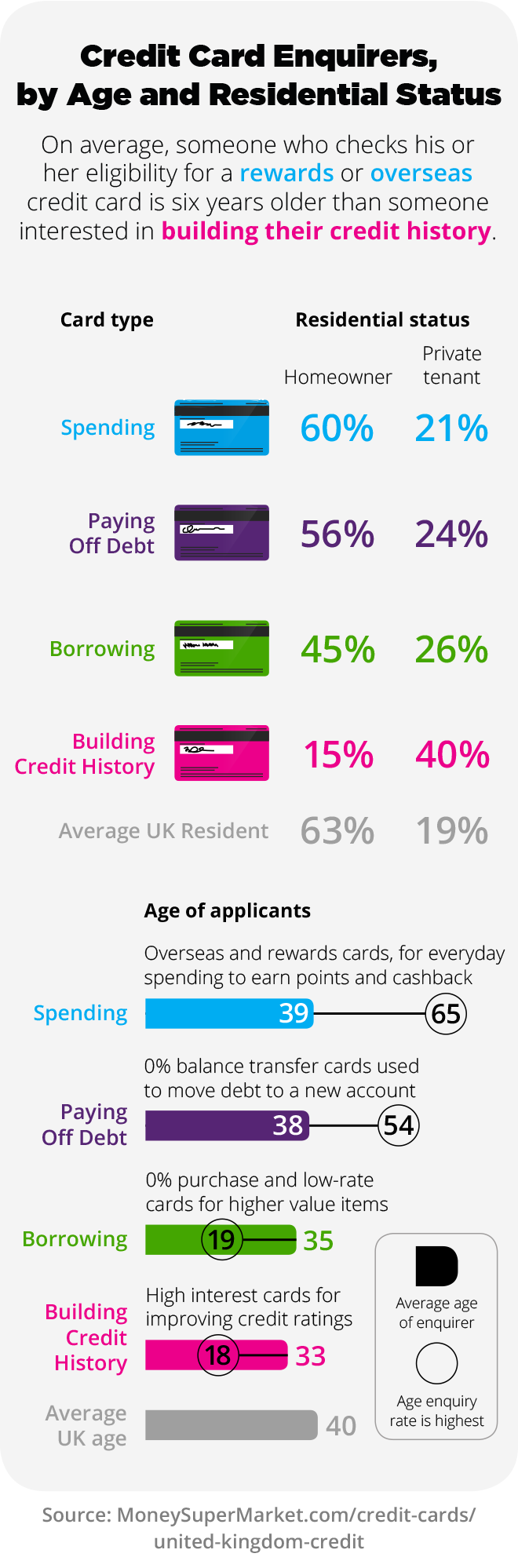

- Paying Off Debt – 0% balance transfer cards, used to move debt to a new account and pay it off without interest

- Borrowing – 0% purchase and low-rate cards, for buying high value items and paying debt over longer periods

- Building Credit History – High interest cards for improving credit ratings due to problems with debt or no borrowing history

- Spending – Overseas and reward cards, used for everyday spending to earn points and cashback

Credit cards designed to help with debt were the most popular type of card overall, accounting for three in ten (28 per cent) enquiries in 2016. A quarter (25 per cent) were for borrowing cards while a fifth (20 per cent) were for credit building and seven per cent for spending.

The most popular time of the week to search for credit cards is 8.15pm on a Monday evening, and enquiries peaked on 22ndJanuary (2016) when 85 per cent more people assessed their eligibility online than a typical day. Overseas cards are the only exception, when enquiries peaked on 6th July.

Enquiries for cards to help manage debt were highest in South Lanarkshire, where 8.1 per 1,000 consumers were looking for cards of this type – 37 per cent higher than the national average. Those checking their eligibility for cards designed to help with debt typically earn £27,456 and are aged 38.

Borrowing cards are favoured by younger consumers, with the highest rate of enquiries amongst those aged 19. Enquiries from Copeland in the North West were 50 per cent higher than in the rest of the country with a rate of 7.8 per 1,000. Rochford (7.5 per 1,000), Dartford (7.1 per 1,000) and Crawley (7.1 per 1,000) also featured in the top ten hotspots.

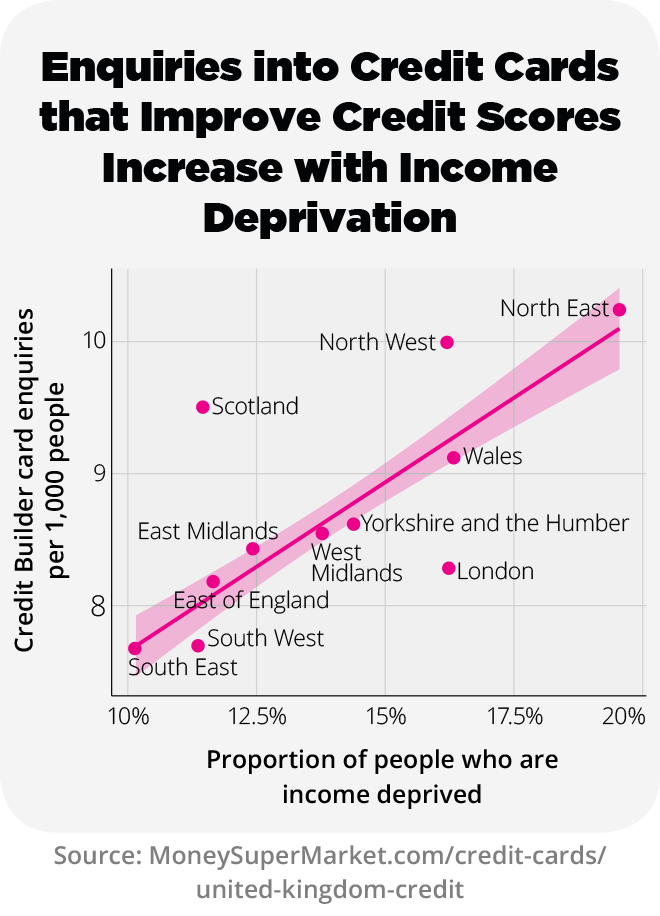

Blackpool is Britain’s credit building hotspot, with the highest rate of enquiries for cards to build credit history (seven per 1,000) at 73 per cent above the national average. Northerners check their eligibility for credit building more frequently (20 per cent) than those in the South, so it’s no surprise five of the top ten local authorities which favour credit building cards are in the North West. A further four are in Scotland, while Corby in the East Midlands also features.

Those aged 18-24 are the most credit conscious, accounting for a quarter (25 per cent) of all enquiries. For every £5,000 less a person earns each year, the popularity of credit building cards increases by five per cent. Consumers earning less than £15,000 a year are 45 per cent more likely to try and build their credit rating than every other income bracket, accounting for 46 per cent of all enquiries about cards of this nature.

London had the highest rate of enquires for spending cards, with nine of the top ten hotspots in the capital. The local authority area, City of London, came in at the top of the table, with 5.9 per 1,000 customers from the area enquiring about this type of card. Those in the North East were least likely to enquire about a spending card.

Two thirds (60 per cent) of customers checking their eligibility for spending cards were men and the average age was 39 – six years older than those typically looking to build credit. Higher earners were also most likely to look at spending cards, as the average salary for people enquiring about this type of card was £34,446 (£47,017 in London). Someone who earned more than £40,000 is 2.7 times more likely to enquire about a spending card than someone who earned less.

Dan Plant, editor-in-chief, MoneySuperMarket, said: “Credit cards can help you save money when managing debt, borrow new funds, build your credit rating or earn rewards for spending. However, you need to select the right type of plastic, and then use it in the right way to maximise the benefit. Otherwise you may face unnecessary charges, damage to your credit rating or a build-up of unwanted debt, which will all make it more difficult to be accepted for new borrowing in future.”

Enjoy the convenience of having The Sunday Post delivered as a digital ePaper straight to your smartphone, tablet or computer.

Subscribe for only £5.49 a month and enjoy all the benefits of the printed paper as a digital replica.

Subscribe